Down in the bottom right hand corner of this blog, I keep a list of Interesting People. Generally, what qualifies someone as sufficiently interesting to make the list is that they have published a collection of works that are worth reading. Someone that I recently added to the list is Michael Mauboussin. He has written some interesting articles in the investing game theory space, and a particularly relevant article on the importance of position sizing (asset allocation) in investing called Size Matters.

The point of that article is that, just because you have a strategy with a positive expectation value, doesn't mean that you should go all in on your first bet. You might lose, and then you'd have nothing. Clearly, this is not the best way to play a game that, in theory, gives you an edge and should allow you play profitably over the long term.

ASX Investor Hour with Jim Berg

Once a month, the ASX run lunch time investor hour seminars in each capital city in Australia, and occasionally, they are worth going to. Today's was called "When you should reinvest and how you should do it" by Jim Berg, and it sounded interesting enough, so I went along.

Before hand though, I checked out his website, and this made me somewhat skeptical of the seminar. Basically, I figured it was going to be a sales pitch, and sure enough, his book was on sale as I entered the foyer and for $30 a month I could subscribe to his newsletter.

Still, I took some notes, so here goes:

Before hand though, I checked out his website, and this made me somewhat skeptical of the seminar. Basically, I figured it was going to be a sales pitch, and sure enough, his book was on sale as I entered the foyer and for $30 a month I could subscribe to his newsletter.

Still, I took some notes, so here goes:

Invest in your health 2

Some videos that I recommend, if, like me, you're a little too tubby:

Beware of the carbs:

Beware of fructose:

Be healthy, be happy.

Beware of the carbs:

Beware of fructose:

Be healthy, be happy.

Gold Symposium Panel Questions

Earlier this week, I attended the Gold Symposium in Luna Park in Sydney. All in all, it was a great couple of days, with great keynote speakers. The final session was Q&A with a panel that included Eric Sprott, John Embry, Ben Davies and Egon von Greyerz. Anyway, there were a couple a questions that were posed to the panel that I don't think they did a great job of answering, and with the benefit of contemplation time, and a text editor, I'd thought I'd give them a shot.

Question 1: If I had invested 1 ounce of gold into the equity market 100 years ago, today it would be worth 1400 ounces (or whatever), yet if I had kept it as gold, it would still only be 1 ounce. So, why should I buy physical gold?

My answer to this is three fold:

Question 1: If I had invested 1 ounce of gold into the equity market 100 years ago, today it would be worth 1400 ounces (or whatever), yet if I had kept it as gold, it would still only be 1 ounce. So, why should I buy physical gold?

My answer to this is three fold:

Money Money Money

If you don't already read and follow FOFOA, you should. He's written a great article on Money.

What I learnt:

What I learnt:

- It is important to consider the functions of money separately. Specifically, that the "unit of measure" can be anything, eg, we could prices things (everything) in units (eg. "Man-days work", Bit Coins, 0-10) irrespective of the transactional currency (eg. AUD, cigarettes) and the store of wealth (works of art, houses).

- Base (government) money, is not the same as credit (bank) money. Base money is the "unit of measure", or the yard stick, or the zero to ten system of pricing things. Changing the amount of base money is different to changing the amount credit money.

- MMT is NQR. Sectoral balance sectoral shmalance.

- Government spending is the main problem. (D'uh!)

- USA is headed for hyper-inflation.

- Gold is the place to be.

Fooled by randomness

As I have briefly mentioned before, I have just finished reading Fooled by Randomness, by Nassim Taleb.

Taleb's take on the investing world is that in the spectrum of skill verses luck, many people attribute the success of successful traders, including the traders themselves, down to skill, whereas Taleb mostly attributes it to luck. Even if the traders have demonstrated "long running" success, Taleb attributes this to survivorship bias rather than skill. He believes that many traders essentially follow a well masked "increase risk until you blow up" strategy, he says that it's only a matter of time until they actually blow up, and there is no point praising those that are yet reach that point.

Taleb's take on the investing world is that in the spectrum of skill verses luck, many people attribute the success of successful traders, including the traders themselves, down to skill, whereas Taleb mostly attributes it to luck. Even if the traders have demonstrated "long running" success, Taleb attributes this to survivorship bias rather than skill. He believes that many traders essentially follow a well masked "increase risk until you blow up" strategy, he says that it's only a matter of time until they actually blow up, and there is no point praising those that are yet reach that point.

Employed Capital

At the right price, any profit producing security could give me an initial rate of return of 40%. The security could be a bond or it could be an equity. Let's use CocaCola as an example, as its earnings growth is quite stable, and has been for some time. So, there is a price as which Coca Cola will give me an initial rate of return of 40%. I chose 40% because that's highly likely to be the "once in a lifetime" buying opportunity.

Fooled by Regression to the Mean

I've just finished reading Fooled by Randomness by Nassim Taleb (Great book BTW). There are many interesting topics covered in the book, but I'd like to pick on the one topic that Taleb doesn't quite get right - that of Regression to the Mean.

Taleb writes:

Taleb writes:

This applies to the height of individuals or the size of dogs. In the latter case, consider that two average sized parents produce a large litter. The largest dogs, if they diverge too much from the average, will tend to produce offspring of the smaller size than themselves, and vice versa. This "reversion" for the large outliers is what has been observed in history and explained as regression to the mean. Note that the larger the deviation, the more important the effect.I've long thought it obvious that "regression to the mean" of populations was a myth. After all, on an evolutionary time scale, the "tree of life" expands (into a tree) rather than reaches equilibrium, at a mean. If it were true, we'd all be the same size, and we are not, therefore it isn't true.

On gold producing no income or dividends...

What's all this nonsense about gold not paying a dividend?

Firstly, let's compare apples with apples, because it doesn't make sense to compare the dividends received from "cash that is lent out" with the dividends received from "gold that is not lent out". If, instead, we compare the "not lent out" assets, then neither cash nor gold will pay any dividends. If you had put both a lump of gold and a suitcase of cash under your bed 50 years ago, neither would have paid out dividends, and the contents under your bed would not have changed - but only one of the two would have preserved its purchasing power.

Now, let's consider the "lent out" scenario. Obviously, cash would only be lent out for a reason, and that reason would be interest payable on the capital - generally as or including dividends. As for gold, does anyone really think that gold that is lent out would not be done so under similar, if not identical arrangements, and not pay dividends, or that a greater quantity would not be returned than was lent out.

If there is anybody that believes this, please lend me your gold at 0%?

Firstly, let's compare apples with apples, because it doesn't make sense to compare the dividends received from "cash that is lent out" with the dividends received from "gold that is not lent out". If, instead, we compare the "not lent out" assets, then neither cash nor gold will pay any dividends. If you had put both a lump of gold and a suitcase of cash under your bed 50 years ago, neither would have paid out dividends, and the contents under your bed would not have changed - but only one of the two would have preserved its purchasing power.

Now, let's consider the "lent out" scenario. Obviously, cash would only be lent out for a reason, and that reason would be interest payable on the capital - generally as or including dividends. As for gold, does anyone really think that gold that is lent out would not be done so under similar, if not identical arrangements, and not pay dividends, or that a greater quantity would not be returned than was lent out.

If there is anybody that believes this, please lend me your gold at 0%?

Three Strawman Investing Strategies

Regular reader and commenter Strawman left an insightful and interesting comment on a recent post about cash in investing strategies. It was such a good comment, and so central to the theme of this blog (the search for the ultimate investing strategy), that I thought that it deserved it's own post.

Strawman starts:

Strawman starts:

I also accept that the strategy of buying into quality companies when the price is good, but holding cash is only one way to make this happen.All good so far. Strawman continues:

Basically your strategy seems to be:That's correct. But let's just clarify a few things. Firstly, the P/E in instantaneous, and changes over time. Every time the market presents you with a price (P), you can calculate the corresponding P/E (based on either last years earnings (E), or sometimes, projected earnings). Therefore, I don't really know what you mean by "real long term P/E". Also, I think that you are trying to use "P/E" as a pure indicator of value, which is not quite right, as it depends on the growth prospects of the company. However, let's assume that you can generate a "value indicator", and, to keep the language consistent within this post, let's call that value indicator "P/E".

STRATEGY1: 'Move my wealth from cash into X when the (real long term) P/E for X is really good'.

Buffettology

Without a doubt, the best book I have ever read on investing is The New Buffettology, by Mary Buffett and David Clark.

I was excited to get this book, and was about learn and understand the investing strategy of the world's richest man (at the time). The lesson was simple enough. Buffett invested in companies with a durable competitive advantage. The book explained that businesses that had a durable competitive advantage were the ones that were most likely to grow into the distant future. It named quite a few of these companies - CocaCola, Gillette, H&R Block, etc.

I was excited to get this book, and was about learn and understand the investing strategy of the world's richest man (at the time). The lesson was simple enough. Buffett invested in companies with a durable competitive advantage. The book explained that businesses that had a durable competitive advantage were the ones that were most likely to grow into the distant future. It named quite a few of these companies - CocaCola, Gillette, H&R Block, etc.

Quality Companies and Simple Investing

One of the reasons that I started this blog was because I thought that I had discovered a simple and effective investing strategy, and that I wanted to explore it further, and share it with friends and like minded people. As I've said before I think that the best investing strategy is to buy quality companies when they're cheap. I've given some quality companies metrics before, and also hinted at what cheap might be, but in this post I want to keep it nice and simple. I will explicitly list some quality companies, and give you and very easy way to determine cheapness.

Cash

I've tried to win this argument before - unsuccessfully - that "cash" is a significant enough concept that it should be a "first class citizen" in an investing model. Finally, I found the words that I wanted, from an interview at Gold Money Research with Detlev Schlichter:

At any moment in time you can hold your wealth in three forms: consumption goods, investment goods or money. With money you can stay on the sidelines, you keep your purchasing power and stay ready to buy consumption and investment goods in the future.They key point here is that "cash" - and I'm using that term, in this context, interchangeably with "money", does have the special power of enabling you to stay on the sidelines, while all other investments may be struck by volatility, cash's purchasing power will remain constant (in the short term) to consumer goods, and independent of the volatility of the investment goods.

Property buyers advocate nails investing rules

Enough people have already written about what a flop The Block was, but the article that drew my attention was the one entitled: Eight property rules broken by The Block, by Mal James, from James Buyers Advocates.

He lists the following property investment rules:

He lists the following property investment rules:

Rule No. 1: You make your money when you buy.I couldn't help but immediately see parallels between James' property investment rules and my own value investing rules.

Rule No. 2: Buy the best position you can

Rule No. 3: Consider your target market, before you start.

Rule No. 4: Don't overcapitalise

Rule No. 5: Amateurs don't make money on renovations - they make money because they are lucky that the market happens to be in an upwards phase.

Rule No. 6: Don't think short term with property unless you like excessive risk.

Rule No. 7: Choose local selling agents who are experienced at your price range, and choose ones that can deal outside the auction process.

Rule No. 8: Substance v puffery

House prices (don't) always go up

At least, Melbourne house prices don't always go up.

From here: http://www.macrobusiness.com.au/wp-content/uploads/2011/08/image002-11.png we get monthly Melbourne house price changes: -1.2, -1.6, -1.8, -1.2, -2.1, -2.1, -2.7.

That adds up to a whopping -12% for the first 7 months of 2011, some of which we have to account for normal winter seasonality.

From here: http://www.macrobusiness.com.au/wp-content/uploads/2011/08/image002-11.png we get monthly Melbourne house price changes: -1.2, -1.6, -1.8, -1.2, -2.1, -2.1, -2.7.

That adds up to a whopping -12% for the first 7 months of 2011, some of which we have to account for normal winter seasonality.

Share Prices - Significant factors affecting

I've recently had a go at trying to determine the most significant factors affecting prices of houses and gold and silver, but now it's time to tackle the difficult one - share prices.

One of the things that makes it difficult is that it's a different answer depending on whether we are talking about an individual company verses an equity index (eg. ASX All Ords).

Let's start with what appears to be the most obvious answer - profitability. The most significant factor affecting the share price of an individual company, and perhaps even the indexes, are their profitability. In general, the more profitable companies are, the higher price they can command.

One of the things that makes it difficult is that it's a different answer depending on whether we are talking about an individual company verses an equity index (eg. ASX All Ords).

Let's start with what appears to be the most obvious answer - profitability. The most significant factor affecting the share price of an individual company, and perhaps even the indexes, are their profitability. In general, the more profitable companies are, the higher price they can command.

Sniper pulls the trigger

A friend and colleague recently described my investing strategy back to me as sniping. I had chosen my target companies, and for each one of them I had identified a target price. The cross-hairs were set and I was ready. The trigger finger was not particularly twitchy, but it was ready to fire the moment that something appeared in the sights.

Anyway, I recently went traveling, and so was pretty much off line for about a month. Knowing that this was going to be the case, I decided that I'd put in some low-ball buy orders on the market before I went, just in case a stock market crash occurred while I was away. I won't be so bold as to say that that was a prediction - well - the crash was, but not the timing.

Anyway, I recently went traveling, and so was pretty much off line for about a month. Knowing that this was going to be the case, I decided that I'd put in some low-ball buy orders on the market before I went, just in case a stock market crash occurred while I was away. I won't be so bold as to say that that was a prediction - well - the crash was, but not the timing.

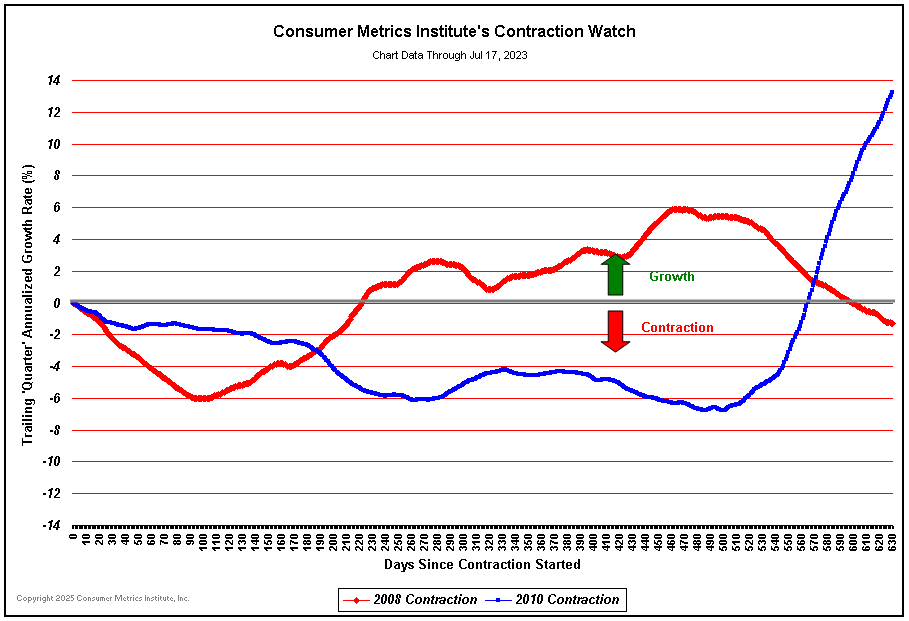

July Consumer Metrics data

I've long been a fan of the Comsumer Metrics Institute. They've been showing the US consumer "double dip" recession for well over a year now - yet the official numbers have only just been "adjusted" to reflect this.

Looking at the latest data, it is surprising to see an uptick that may indicate the end of the contraction.

Perhaps there is light at the end of the tunnel. Time will tell. The Consumer Metrics Institute will probably give a leading indicator either way..

Looking at the latest data, it is surprising to see an uptick that may indicate the end of the contraction.

Perhaps there is light at the end of the tunnel. Time will tell. The Consumer Metrics Institute will probably give a leading indicator either way..

Antal Fekete

Fekete's articles - an interesting read on gold, futures, and what the USD end game might look like.

Gold and Silver prices - Significant factors affecting

Following on from my look at the most significant factors affecting house prices, I would now like to take a look at the gold and silver, and the factors that most affect their prices. (Update: See also: significant factors affecting share prices).

Like with house prices, I'm trying to determine what has the largest impact on their price over the long term, rather than the factors that cause their volatility, as I'm long term investor.

I don't claim to be an expert on the precious metals, but that's never stopped me from having an investment opinion before, so here goes.

Like with house prices, I'm trying to determine what has the largest impact on their price over the long term, rather than the factors that cause their volatility, as I'm long term investor.

I don't claim to be an expert on the precious metals, but that's never stopped me from having an investment opinion before, so here goes.

House Prices - Significant Factors

My plan is to make this a multi-part series, where I take a look at various classes of assets, and the most significant factors that determine or influence their prices. Today I'll look at house prices. Later, I'll take a look at stock market share prices (Update: See here), and I also hope to take a look at gold and silver prices at some stage as well (Update: See here).

So, what are the factors that affect house prices, in order of significance? As an investor, and as a potential home owner, understanding these factors are crucial to making a sensible and profitable investment decision, yet the answers far from clear, and rarely understood. Here's my take on it.

So, what are the factors that affect house prices, in order of significance? As an investor, and as a potential home owner, understanding these factors are crucial to making a sensible and profitable investment decision, yet the answers far from clear, and rarely understood. Here's my take on it.

The problem with "averaging in"

A popular approach to buying shares is set "buy" thresholds. It's a fairly simple approach - when the share prices falls to reach the threshold price, you buy some shares. Often, there are multiple buy point thresholds, such that as the share price falls through each of the threshold, you buy more shares. The theory is that if you thought that the share price was cheap at say $5, then when it hits $4.50, it must be even better value, and so a better buying opportunity.

The theory is not wrong, it is just not optimal.

The theory is not wrong, it is just not optimal.

The Term Deposit Investing Model

It's been a while, so here's another thought experiment.

Suppose that a bank occasionally offered term deposit accounts at extraordinarily good interest rates - say 20% (for ever). Suppose also, that they only did so very rarely - once every 5-10 years. The catch is of course that it's very difficult to get money into this term deposit, as they only accept small denominations, so you have to manually keep filling out application forms so that you can get as much money in as possible, and you have to do so for the limited time that the bank will accept the applications.

Suppose that a bank occasionally offered term deposit accounts at extraordinarily good interest rates - say 20% (for ever). Suppose also, that they only did so very rarely - once every 5-10 years. The catch is of course that it's very difficult to get money into this term deposit, as they only accept small denominations, so you have to manually keep filling out application forms so that you can get as much money in as possible, and you have to do so for the limited time that the bank will accept the applications.

Getting left behind

Another dinner party on the weekend, and so another chance to make some observations about people's beliefs about the Australian property market.

One guy made the (somewhat typical) following comments:

One guy made the (somewhat typical) following comments:

- If you don't buy now, you're going to get left behind.

- If not now, then when? Prices are only going to go up.

Price to Book ratio and Return on Equity

Following on from my look at the Price to Earnings ratio, and in a similar vein to my post on subsequent rates of return, I'd now like to take a look at P/B ratios and ROE. The mechanics of the numbers are fairly straight forward.

The Price to Book ratio is the price that you pay for the book value of the company - the book value being the net (booked) value of their assets - or in really simplistic terms - how much money they have in the bank, assuming no liabilities. So, if they have $100,000 in assets and you pay $200,000 for the company, you are paying a price to book value of 2:1.

The Return on Equity is simply how efficient the company is at making a profit. If they use the $100,000 to generate $15,000 profit, they have an ROE of 15%. Not bad.

These two metrics are linked though the P/E ratio.

The Price to Book ratio is the price that you pay for the book value of the company - the book value being the net (booked) value of their assets - or in really simplistic terms - how much money they have in the bank, assuming no liabilities. So, if they have $100,000 in assets and you pay $200,000 for the company, you are paying a price to book value of 2:1.

The Return on Equity is simply how efficient the company is at making a profit. If they use the $100,000 to generate $15,000 profit, they have an ROE of 15%. Not bad.

These two metrics are linked though the P/E ratio.

Australian Housing Bubble - Change in Debt

Here is a link to Steve Keen's recent presentation to a debate re the Australian Property Market

Some essential points from the video (with data to back them up):

Some essential points from the video (with data to back them up):

- It's not population growth or sluggish construction that drives house prices.

- Money pressure and booming credit drives house prices.

- Stagnant credit causes house prices to go down.

- Accelerating mortgage debt leads house prices by 2-4 months.

- Australia has a bigger housing bubble than the US had.

- Australian banks are not responsible lenders than the American banks, nor are they more financially sound.

- "It's not people that buy houses, it's people with mortgages that buy houses."

- "Rising house prices require accelerating debt."

- "The first home vendor's boost, when the government gave $7,000 to first home buyers, who then leveraged it up at the bank, and bid $100,000 extra dollars more, and handed it over to the vendors."

- "We are in the biggest, debt financed, asset bubble in human history, and I'm afraid, I think you'll ignore it at your peril."

Invest in your health

I'm drawing a long bow today with relevance to investing, however, for me personally, the whole point of investing is about having the time and resources to enjoy life with your family and friends. It goes without saying that to be able to really enjoy life, you need to be healthy.

Hat tip to Schedule Flow for point me to this video. I highly recommend that you watch it.

Hat tip to Schedule Flow for point me to this video. I highly recommend that you watch it.

Super Fees

I've been meaning to write about fund management fees for a while now, however these articles covered most of what I had to say, so I didn't bother - until now. Just yesterday, I saw an ad on TV that talked about how having multiple superannuation accounts can lead to excess fees, and it reminded me of one of the biggest problems that I have with fund managers.

It's not the breadth of your accounts that leads to excess fees - it's the depth. Let me explain..

It's not the breadth of your accounts that leads to excess fees - it's the depth. Let me explain..

Price Earnings Ratio

The Price Earnings (P/E) Ratio is a well known and easily computed number regarding the value of a company. Yet, it's really not that well understood. What exactly does a P/E of 14 indicate? Is it better, or worse than a P/E of 16?

The way I see it, there are two main components that make up the P/E ratio, and they are not price and earnings - well, they are - but, if you slice it another way then you get two more revealing components.

The way I see it, there are two main components that make up the P/E ratio, and they are not price and earnings - well, they are - but, if you slice it another way then you get two more revealing components.

Quality Company Metrics

The first step in my investing strategy is to identify quality companies. There are approximately 2000 companies listed on the ASX, and I only want to invest in the top handful - and even then - only when they are cheap. But back to step 1, I'd like to walk you through how I identified the few companies at the top of the list.

I started by downloading all of the relevant company financial data from Comsec. Note that this was not the price history for the companies, but each company's financial reporting history.

I started by downloading all of the relevant company financial data from Comsec. Note that this was not the price history for the companies, but each company's financial reporting history.

Inflation

I've been thinking about inflation a lot lately. Some time ago, I realised that I had no understanding of what inflation was all about, and I was somewhat embarrassed by this knowledge gap. Since then, I've tried to build a model of understanding for inflation, and it goes something like this...

Subsequent Rates of Return

The concept of initial rate of return (IRR) is fairly straight forward and easy to understand. Related, but not so straight forward, to the initial rate of return, is the subsequent rates of return (no particular acronym) that apply in the periods following the initial rate of return.

The Evil Princes of Martin Place

I've (finally) just finished reading The Evil Princes of Martin Place by Chris Leithner. It took me quite a while to finish, primarily because I haven't had that much time to read lately, but also because it's not an easy book to skim - I really had to concentrate.

Overview of The Evil Princes of Martin Place

In the book, Leithner presents a history of banking and money, analyzes the causes of depressions and recessions, describes the failings of the banking system, including the central banks and governments that support them, and comes up with some fixes for the problems that he sees.

Some specific conclusions that Leithner reaches in the book are:

Overview of The Evil Princes of Martin Place

In the book, Leithner presents a history of banking and money, analyzes the causes of depressions and recessions, describes the failings of the banking system, including the central banks and governments that support them, and comes up with some fixes for the problems that he sees.

Some specific conclusions that Leithner reaches in the book are:

Bubbles

A friend recently asked me about the shape of bubbles. He wanted to know how long the Australian property market crash would last. (Note that the question wasn't about whether or not the Australian property market was in a bubble, nor whether or not it would crash - they were both givens. The question was simply whether the crash would be swift and brutal, or long and drawn out).

Baskets of Goods

Bananaman lives in Barterland. Bananaman grows bananas for a living, and often travels to the Barterland market where he swaps his bananas for other goods.

Bananaman is clever. He suspects that the Barterlandians are slowly thinking less and less of his bananas, but he's not quite sure, because many of the other goods are seasonal as well, so there is rarely any consistency between the number of apples or oranges that he gets for his bananas, but lately he's feeling as though he's just not getting as many swapped goods as he used to.

Bananaman is really clever. He devises a scheme, whereby he creates a basket of goods that he likes, including apples and oranges and other juicy things, and over time, he'll track how many bananas he has to swap to get the goods that he likes.

Bananaman is clever. He suspects that the Barterlandians are slowly thinking less and less of his bananas, but he's not quite sure, because many of the other goods are seasonal as well, so there is rarely any consistency between the number of apples or oranges that he gets for his bananas, but lately he's feeling as though he's just not getting as many swapped goods as he used to.

Bananaman is really clever. He devises a scheme, whereby he creates a basket of goods that he likes, including apples and oranges and other juicy things, and over time, he'll track how many bananas he has to swap to get the goods that he likes.

Making every post a winner

There is an expression in sports races: "Making every post a winner". By trying to race to every post along the way, the racer is going as fast as they can, and it is only a matter of time before they tire, because you can't go 100% all the way - unless you are very close to the end of the race already.

In races like the Tour De France, you generally never see the cyclists going 100%. For the most part, they wait, and wait, and wait, until the "key moment", and only at that time do you see them going flat out, and the race is won and/or lost in those very few key moments.

Similarly, in investing, the best strategy is not to make every "day" a winner, or every "week", or even every "month", "quarter" or "year".

In races like the Tour De France, you generally never see the cyclists going 100%. For the most part, they wait, and wait, and wait, until the "key moment", and only at that time do you see them going flat out, and the race is won and/or lost in those very few key moments.

Similarly, in investing, the best strategy is not to make every "day" a winner, or every "week", or even every "month", "quarter" or "year".

Compounding Engines and Price Volatility

I view companies as compounding engines.

Quality companies have consistently high returns on equity. They have this special ability to use their retained earnings to increase their equity base, which they can then use to generate even more earnings in the future, and so on. I don't give any consideration to low quality companies, that is, that don't have consistent and high returns on equity, so pour moi, and long term value investors alike, it holds that companies are compounding engines.

Quality companies have consistently high returns on equity. They have this special ability to use their retained earnings to increase their equity base, which they can then use to generate even more earnings in the future, and so on. I don't give any consideration to low quality companies, that is, that don't have consistent and high returns on equity, so pour moi, and long term value investors alike, it holds that companies are compounding engines.

Follow the yellow brick road

Something slightly off-track this week. I recently saw a documentary called The Secret of Oz. It suggests that the author of the original version of the Wonderful Wizard of Oz, Frank Baum, based the book on American monetary history. In case you're confused - yes - I am talking about the book with Dorothy, the wicked witches, and the yellow brick road.

Empire Investing Strategy Review - Part 2

In the first part of this review, I looked at the first two components of the investing strategy outlined at the Empire Investing website. These were the 1. Filter and 2. Value steps. I'd now like to take a look at the next few:

Assign Risk - ustilise a margin of safefy

I've never quite got the concept of "margin of safety". I understand that estimations and predictions have a margin of error, and that by creating a margin of safety, one hopes to eliminate, or at least minimize, the risk of a negative outcome. However, what I can't grasp is how this is any different to the concept of maximizing expectation value, or in layman's terms "trying to make as much money as possible", and hence why it's referred to as "margin of safety" rather than "maximizing profits".

I've leave "6. Assign Capital" for another post, as I think that that is complex enough to warrant it's own post.

- 3. Assign Risk - utilise a margin of safety.

- 4. Observe - Concentrate and watch the select few closely - like a hawk.

- 5. Act on Buy Signals - Purchase on every buy signal.

Assign Risk - ustilise a margin of safefy

I've never quite got the concept of "margin of safety". I understand that estimations and predictions have a margin of error, and that by creating a margin of safety, one hopes to eliminate, or at least minimize, the risk of a negative outcome. However, what I can't grasp is how this is any different to the concept of maximizing expectation value, or in layman's terms "trying to make as much money as possible", and hence why it's referred to as "margin of safety" rather than "maximizing profits".

Is there a little book that beats "The little book that beats the market"?

Recently, I looked at the little book that (still) beats the market.

Being a revised edition of the orignal (hence the "still" in the title), towards the end of the book, Greenblatt responds to suggestions for improvements to his magic formula. Interestingly, he tried a number of these suggested improvements using his simulation tool, and despite sounding like good ideas, none of the suggestions actually improved the portfolio performance.

This reminded me of the classic iterated prisoner's dilemma competition, where the simple winner (tit-for-tat) of the first competition also won the second competition, despite all the new entrants in the second competition knowing exactly how it worked to win the first competition, and being written to specifically beat tit-for-tat. Each of the so-called "improvements" on tit-for-tat could beat tit-for-tat, but couldn't outperform tit-for-tat on average against all of the other strategies.

So, I pose the question - can the magic formula be improved, or does it's elegant simplicity outperform any variation?

Being a revised edition of the orignal (hence the "still" in the title), towards the end of the book, Greenblatt responds to suggestions for improvements to his magic formula. Interestingly, he tried a number of these suggested improvements using his simulation tool, and despite sounding like good ideas, none of the suggestions actually improved the portfolio performance.

This reminded me of the classic iterated prisoner's dilemma competition, where the simple winner (tit-for-tat) of the first competition also won the second competition, despite all the new entrants in the second competition knowing exactly how it worked to win the first competition, and being written to specifically beat tit-for-tat. Each of the so-called "improvements" on tit-for-tat could beat tit-for-tat, but couldn't outperform tit-for-tat on average against all of the other strategies.

So, I pose the question - can the magic formula be improved, or does it's elegant simplicity outperform any variation?

In case you missed it...

This blog is now three months old, so I thought that it might be time for a checkpoint review.

I started off by trying to talk about some tax effective investment structures, in the hope that some real and useful information would give me some online credibility. Perhaps I waited too long between the actual setup of those structures and the documentation thereof, and so the accuracy, and hence usefulness was not quite as high as I had hoped. I'll know better for next time.

I tried a couple of thought experiments, which I personally found very useful in drawing me to a couple of my key investment beliefs, but they were not well received - in terms of readership and participation. Nevertheless, I will persist with these, as I have a number more to go through, and they are central to the theme of this blog - delusional investing: "These are the thoughts going through my head. Am I delusional?"

There were a few other random posts, that don't directly relate to the theme of this blog, but that I needed to write about to understand myself. There will be many more these, that one day, I hope to string together into a reasonably cohesive story.

The most popular post to date has been on the little book that beats the market. I'm not sure that this is a great thing, because I haven't been able to determine if the people that search for that book are after the "quick win" investing answer, or whether they are genuinely interesting in investing strategies. Hopefully the latter, because I'll continue to review investing strategies as I find them.

Ideally, I like to have more comments on my posts than I have been receiving so far. I don't measure the success of this blog on the number of views, but instead, on the number of "insightful comments". Having only received a handful of comments, I have to count this as a failure of this blog to date. Thanks to those that have commented though.

I think that I need to get more involved with other value investing blogs, and to participate in the existing communities, to be able to get the feedback that I am looking for. To that end, I hope to review a bunch of blogs to determine which ones are of value to me, in the hope of reciprocity.

Anyway, thanks for reading, and please give feedback.

I started off by trying to talk about some tax effective investment structures, in the hope that some real and useful information would give me some online credibility. Perhaps I waited too long between the actual setup of those structures and the documentation thereof, and so the accuracy, and hence usefulness was not quite as high as I had hoped. I'll know better for next time.

I tried a couple of thought experiments, which I personally found very useful in drawing me to a couple of my key investment beliefs, but they were not well received - in terms of readership and participation. Nevertheless, I will persist with these, as I have a number more to go through, and they are central to the theme of this blog - delusional investing: "These are the thoughts going through my head. Am I delusional?"

There were a few other random posts, that don't directly relate to the theme of this blog, but that I needed to write about to understand myself. There will be many more these, that one day, I hope to string together into a reasonably cohesive story.

The most popular post to date has been on the little book that beats the market. I'm not sure that this is a great thing, because I haven't been able to determine if the people that search for that book are after the "quick win" investing answer, or whether they are genuinely interesting in investing strategies. Hopefully the latter, because I'll continue to review investing strategies as I find them.

Ideally, I like to have more comments on my posts than I have been receiving so far. I don't measure the success of this blog on the number of views, but instead, on the number of "insightful comments". Having only received a handful of comments, I have to count this as a failure of this blog to date. Thanks to those that have commented though.

I think that I need to get more involved with other value investing blogs, and to participate in the existing communities, to be able to get the feedback that I am looking for. To that end, I hope to review a bunch of blogs to determine which ones are of value to me, in the hope of reciprocity.

Anyway, thanks for reading, and please give feedback.

The reality of models

Models are useful abstractions of reality. The "correctness" of a model is simply is usefulness for a particular purpose.

Instrinsic Value and Target Prices

When I was recently reviewing Empire Investing, I luckily stopped at the "value" step of their investment strategy, as this gave me time to reflect on a couple of things.

The first is the concept of intrinsic value, which most value investors will know well, as the traditional texts of Benjamin Graham and Warren Buffett refer to it often. I, however, don't subscribe to it. I simply don't believe that anything has an "intrinsic value" - the only "value" that can be placed upon something is someone's desire to have it.

A long term investor will value certain properties of a company very differently than a short term investor would value those properties.

Consider the example of a house. I could describe a house as "2 bedrooms, 1 bathroom, modern and in a nice suburb" to a room full of people, and ask each of them to create a baseline valuation of this house. It doesn't matter what valuation they come up with. I could then ask "and what is the change in value if I add a double-car lock-up garage on". To some people, this might de-value the house, (if for example they didn't have a car, didn't want one, and didn't need the storage space) and to others, like myself, it would add value to the house. So, what is the "intrinsic value" of the garage? It doesn't make sense.

So, what Buffett et al are referring to when they refer to intrinsic-value is actually value-to-them, as long term investors.

The first is the concept of intrinsic value, which most value investors will know well, as the traditional texts of Benjamin Graham and Warren Buffett refer to it often. I, however, don't subscribe to it. I simply don't believe that anything has an "intrinsic value" - the only "value" that can be placed upon something is someone's desire to have it.

A long term investor will value certain properties of a company very differently than a short term investor would value those properties.

Consider the example of a house. I could describe a house as "2 bedrooms, 1 bathroom, modern and in a nice suburb" to a room full of people, and ask each of them to create a baseline valuation of this house. It doesn't matter what valuation they come up with. I could then ask "and what is the change in value if I add a double-car lock-up garage on". To some people, this might de-value the house, (if for example they didn't have a car, didn't want one, and didn't need the storage space) and to others, like myself, it would add value to the house. So, what is the "intrinsic value" of the garage? It doesn't make sense.

So, what Buffett et al are referring to when they refer to intrinsic-value is actually value-to-them, as long term investors.

Empire Investing Strategy Review - Part 1

This blog is supposed to be about investing strategies, and to date, I haven't spent too much time talking about them (other than the magic formula). Luckily for us, there is an investment company called Empire Investing that publishes their investing strategy, and so today I'd like to review it.

Let me start by saying that I have no affiliation with Empire or any of it's staff, other than that The Prince has chanced across this blog before. Not that it matters though, as it seems that they are not currently accepting any new clients or funds.

So, to start off, I'd say that one of the reasons that I'm looking forward to this review is that their investing strategy is quite similar to my own, but with some interesting differences. Let's look at their strategy in a nut shell:

Let me start by saying that I have no affiliation with Empire or any of it's staff, other than that The Prince has chanced across this blog before. Not that it matters though, as it seems that they are not currently accepting any new clients or funds.

So, to start off, I'd say that one of the reasons that I'm looking forward to this review is that their investing strategy is quite similar to my own, but with some interesting differences. Let's look at their strategy in a nut shell:

The stock market side pot

Here's another thought experiment for you.

Suppose the government (or the stock exchange) changed the rules on investing to ban short-term trading. The mechanism for how they do this is not important, but it could be implemented, for example, by changing the capital-gains tax rules to tax short term trades at 100%, making them pointless. Let's say that they effectively prevented anyone from owning stocks for less than 3 years.

What would happen to the market?

Suppose the government (or the stock exchange) changed the rules on investing to ban short-term trading. The mechanism for how they do this is not important, but it could be implemented, for example, by changing the capital-gains tax rules to tax short term trades at 100%, making them pointless. Let's say that they effectively prevented anyone from owning stocks for less than 3 years.

What would happen to the market?

Friday on my mind - continued

I hope that you've had some time to think about the original thought experiment. Please read it if you haven't, or else the rest of this post will make no sense whatsoever.

Friday on my mind

Here's a thought experiment for you.

Suppose that you own a regular house in a regular suburb. One Sunday, you wake up, and you think to yourself - "I like this house, I think it's worth $500,000. Yes, I wouldn't sell it for any less than that."

On Monday morning, for whatever reason - it doesn't actually matter why - your next door neighbour, who's house is practically identically to yours, comes over to your house and says "Today I am leaving, and I'm giving you my house. Here's the title. It's yours".

On Tuesday morning, a man appears at you door, and offers you $500,000 for your house. You seriously consider it, and tell him that you'll think about it, and get back to him. You also point out that you own the house next door. He leaves you with his offer.

Suppose that you own a regular house in a regular suburb. One Sunday, you wake up, and you think to yourself - "I like this house, I think it's worth $500,000. Yes, I wouldn't sell it for any less than that."

On Monday morning, for whatever reason - it doesn't actually matter why - your next door neighbour, who's house is practically identically to yours, comes over to your house and says "Today I am leaving, and I'm giving you my house. Here's the title. It's yours".

On Tuesday morning, a man appears at you door, and offers you $500,000 for your house. You seriously consider it, and tell him that you'll think about it, and get back to him. You also point out that you own the house next door. He leaves you with his offer.

The buy, hold, sell investment strategy review

In analyzing an investment strategy, a simple but useful thing that I like to do is apply my "three boxes" test to it. In itself, the 3 boxes test is quite simple, but it has some key concepts that quite a number of people that I have tried to explain this to find difficult to grasp. The 3 boxes are "buy", "hold", and "sell", and I tick the box if the strategy tries to make money in that particular action.

Not everyone accepts that there are 3 opportunities to make money in every investment. You will often here the quote "It's only paper money until you've locked in your profits", and hence there is only one opportunity to make money - and that is when you sell and lock the profits in.

This line of thinking comes from 2 main sources. Firstly, there is the accountants view, that says that until a "capital gains event" has triggered, you can't actually book your profits. Similarly, the day-traders focus on market price, that zigs and zags so often that a particular zag is meaningless unless you sell, because it could zig in the next minute, wiping out you profits, and therefore, if you don't sell to lock in your profits, they could disappear in a puff of smoke.

I think that this view is very limited, and that it is for more useful to consider the 3 opportunities. So, how do you make money in each of the buy/hold/sell opportunities? Let's look at each individually.

To make money when you "buy" something,

Not everyone accepts that there are 3 opportunities to make money in every investment. You will often here the quote "It's only paper money until you've locked in your profits", and hence there is only one opportunity to make money - and that is when you sell and lock the profits in.

This line of thinking comes from 2 main sources. Firstly, there is the accountants view, that says that until a "capital gains event" has triggered, you can't actually book your profits. Similarly, the day-traders focus on market price, that zigs and zags so often that a particular zag is meaningless unless you sell, because it could zig in the next minute, wiping out you profits, and therefore, if you don't sell to lock in your profits, they could disappear in a puff of smoke.

I think that this view is very limited, and that it is for more useful to consider the 3 opportunities. So, how do you make money in each of the buy/hold/sell opportunities? Let's look at each individually.

To make money when you "buy" something,

The little book that beats the market - still

I've just finished reading the little book that still beats the market, by Joel Greenblatt. It's written in a very unique and quirky style that resonates well with me. The magic formula that he documents is a value investing strategy worthy of review. He very eloquently describes it as "systematically finding above-average companies at below average prices".

The essence of Grenblatt's magic formula is to rank each company by 2 criteria. The first criteria is "quality", for which he uses return on capital, and the second criteria is "cheapness", for which he uses earnings yield. As point of detail, for return on capital he uses EBIT/(Net Working Capital + Net Fixed Assets), and for earnings yield he uses EBIT/Enterprise Value.

The essence of Grenblatt's magic formula is to rank each company by 2 criteria. The first criteria is "quality", for which he uses return on capital, and the second criteria is "cheapness", for which he uses earnings yield. As point of detail, for return on capital he uses EBIT/(Net Working Capital + Net Fixed Assets), and for earnings yield he uses EBIT/Enterprise Value.

The challenge of changing one's investing model

Models are hard to build. Not only that, if your model is built upon poor foundations, it may be forever doomed to be a poor performer, and no amount of tweaking will ever resolve this. Emotionally, it can be very difficult to throw out an entire model and start again.

This is the biggest difficulty I encounter when trying to explain value investing to people. It contradicts so much of what they know about investing that it initially very difficult to accept. This difficultly is worsened by the amount of "experience" that the person has.

This is the biggest difficulty I encounter when trying to explain value investing to people. It contradicts so much of what they know about investing that it initially very difficult to accept. This difficultly is worsened by the amount of "experience" that the person has.

Measuring Portfolio Performance

It sounds like a simple topic - measuring portfolio performance - so why do so few investors, both amateur and professional, do it so poorly?

The answer should be simple: The way to measure portfolio performance is annual compounding rate of return.

So, how (and why) does it get complicated?

Firstly, many investors are not proud of their performance, and will therefore try and mask their poor performance. This comes in many forms:

The answer should be simple: The way to measure portfolio performance is annual compounding rate of return.

So, how (and why) does it get complicated?

Firstly, many investors are not proud of their performance, and will therefore try and mask their poor performance. This comes in many forms:

- Reporting only the highlights: "Fund manager of 2010".

- Reporting over a shorter time-frame than the fund has existed: "20% last year"

- Reporting cumulative results rather than annual results: "80% over last 10 years"

- Erroneously averaging yearly results. Eg, +20 and -20 does not average 0.

- Reporting "relative" performance, rather than actual: "Outperformed market (-15%) by 3%"

- Reporting without consideration to inflation.

Gambling

I have briefly written about definitions before, and how it is silly to argue over them. Yet, I can't help but get into arguments about the definition of "gambling" with people.

My definition is gambling is fairly broad, and, using this definition, people gamble all the time. Thus people that believe that they "don't gamble" struggle to accept my definition. In fact, it was a former colleague refusing to enter to the work footy-tipping competition (for which there was no entry fee and no prize money) because she "didn't gamble", that got me thinking about this in the first place.

This struck me as flawed thinking for two reasons. Firstly, because no money was changing hands, and secondly, because I didn't think it was possible to "not gamble".

My definition is gambling is fairly broad, and, using this definition, people gamble all the time. Thus people that believe that they "don't gamble" struggle to accept my definition. In fact, it was a former colleague refusing to enter to the work footy-tipping competition (for which there was no entry fee and no prize money) because she "didn't gamble", that got me thinking about this in the first place.

This struck me as flawed thinking for two reasons. Firstly, because no money was changing hands, and secondly, because I didn't think it was possible to "not gamble".

Summary: A top down look at the year ahead, Saul Eslake

Here's a quick summary of the following ASX Investor hour presentation.

Topic: A top down look at the year ahead, Saul Eslake, Grattan Institute

Australian Economy:

Topic: A top down look at the year ahead, Saul Eslake, Grattan Institute

Australian Economy:

- Linked to mining, which is linked to China.

- Australian is the only country to supply 3 main China commodities: Iron Ore, Coal, Gas.

- Strength to continue for a number of years.

- Low government debt compared to other "Advanced" economies.

- Does not see much growth in 2011

- But does not think that a crash is likely

- Will see growth beyond 2011.

- Does not see inflation in the near future as a major problem.

- Thinks they will remain constant for 6 months

- Maybe 1 or 2 rises later in 2011.

Paper Money

What is paper money? And, more specifically what are "paper profits" and "paper losses"?

Recently, I was watching this video, when John, the author, used the term "paper money" to refer to "cash" as well as "contracts", because both were printed on paper. (Ignore that cash is now printed on plastic).

Now, as I've said before, I'm not one to be picky about definitions, but I do take note when I think that someone is using a definition that seems different to my own, as well as being different to what I believe is common usage.

My understanding of "paper money", and again, more specifically, "paper profits" and "paper losses", is that it refers to unrealised capital gains. For example, when an asset that you own temporarily doubles in price, you have a "paper profit" of 100%. The term "paper" is used because a) the asset (eg stock) price, was published in the newspaper, and b) because when you update your personal "paper" balance sheet to reflect the updated market price, you write down the 100% profit.

In this way, neither "cash" nor "contracts of ownership" are considered "paper" money.

Why is this important?

Because the whole concept of "market value", and, more specifically, the extrapolation of the market value of the most-recently transacted shares to the total value of all the shares, ie, "market capitalisation", I believe to be erroneous. I hope to cover the details of that belief sometime in the near future.

But for now, in conclusion, thinking that "paper profits" are real is somewhat delusional..

Recently, I was watching this video, when John, the author, used the term "paper money" to refer to "cash" as well as "contracts", because both were printed on paper. (Ignore that cash is now printed on plastic).

Now, as I've said before, I'm not one to be picky about definitions, but I do take note when I think that someone is using a definition that seems different to my own, as well as being different to what I believe is common usage.

My understanding of "paper money", and again, more specifically, "paper profits" and "paper losses", is that it refers to unrealised capital gains. For example, when an asset that you own temporarily doubles in price, you have a "paper profit" of 100%. The term "paper" is used because a) the asset (eg stock) price, was published in the newspaper, and b) because when you update your personal "paper" balance sheet to reflect the updated market price, you write down the 100% profit.

In this way, neither "cash" nor "contracts of ownership" are considered "paper" money.

Why is this important?

Because the whole concept of "market value", and, more specifically, the extrapolation of the market value of the most-recently transacted shares to the total value of all the shares, ie, "market capitalisation", I believe to be erroneous. I hope to cover the details of that belief sometime in the near future.

But for now, in conclusion, thinking that "paper profits" are real is somewhat delusional..

Dividend Reinvestment Plans

There are many companies that offer dividend reinvestment plans. These are "automatic share buy orders". Instead of receiving dividends from the company in the form of cash, you will receive shares, generally purchased at the current market price.

I will never participate in a dividend reinvestment plan. The reason is simple. To me, a good investment strategy will only buy assets when they are cheap. Any given "now", without any consideration of price, is not likely to be cheap. So, you may end up buying shares when they are not cheap, or, at worst, when they are bloody expensive.

So, why then do so many companies offer a dividend reinvestment plan?

Well, I think it is a cheap management trick to pump up the share price. If a company can cause a continual buying trend, share prices will tend to rise (until the scales tip back towards balancing with earnings).

The problem though, is that management should not be concerned with the price of the company shares. "Ahhh, but they are!" I hear you say. And you're right. Often Executive bonuses are linked to the share price of the company. This is stupid. Shareholders should let management focus on the profitability and growth of the company, and then the share price will take care of itself. If shareholders vote for short-term reward structures, they will get short-term focused management - to the detriment of the long term performance of the company.

The problem with short-term focused management should be obvious. CEOs that maximize their bonus before walking out the door leaving a hell of a mess behind. This is definitely not in the interest of shareholders.

So, as a shareholder:

(KX9UC8U9WVYT)

I will never participate in a dividend reinvestment plan. The reason is simple. To me, a good investment strategy will only buy assets when they are cheap. Any given "now", without any consideration of price, is not likely to be cheap. So, you may end up buying shares when they are not cheap, or, at worst, when they are bloody expensive.

So, why then do so many companies offer a dividend reinvestment plan?

Well, I think it is a cheap management trick to pump up the share price. If a company can cause a continual buying trend, share prices will tend to rise (until the scales tip back towards balancing with earnings).

The problem though, is that management should not be concerned with the price of the company shares. "Ahhh, but they are!" I hear you say. And you're right. Often Executive bonuses are linked to the share price of the company. This is stupid. Shareholders should let management focus on the profitability and growth of the company, and then the share price will take care of itself. If shareholders vote for short-term reward structures, they will get short-term focused management - to the detriment of the long term performance of the company.

The problem with short-term focused management should be obvious. CEOs that maximize their bonus before walking out the door leaving a hell of a mess behind. This is definitely not in the interest of shareholders.

So, as a shareholder:

- I will always vote against the introduction of a dividend reinvestment plan.

- I will be wary of any management that suggest the introduction of a dividend reinvestment plan.

- I will always vote against executive remuneration linked to short term objectives, such as share price.

- I will never participate in dividend reinvestment plans.

(KX9UC8U9WVYT)

Family Trusts

Disclaimer: I am not a lawyer. I am not an accountant. I am not a financial adviser. The description below is written in layman's terms, by a layman. It may not be accurate. Seek professional advice.

At about the same time that I setup my SMSF, at the advice of my accountant, I also setup a Family Trust.

A Family Trust is similar in structure to the SMSF, in the sense that it a legal entity, essentially created by the existence of a deed document. It can own assets.

So, why setup a Family Trust?

A Family Trust allows me to distribute any income received by the Family Trust to the beneficiaries of the Trust in a discretionary manner. The beneficiaries of the Trust are the people (generally immediate family members) that can receive income generated by the Trust.

The real advantage of the Family Trust is the discretionary nature by which income can be allocated. Basically, income can be allocated as required (or, at the sole discretion of the Trustees) as to maximize the net benefit (ie, after tax) to the beneficiaries.

So, in my case, my partner and I will likely alternate being the primary income earner and the primary care giver across a number of years. Using the Family Trust structure, we simply put the name of the income earning assets into the name of the Trust, and can then (in any given tax year, and changing between tax years) allocate income to primary care giver first, ensure that we maximize our net earnings.

We can also allocate $3,000 per year to each child, without paying any tax on that income.

You should be able to see the effectiveness of the Family Trust structure, in building and maintaining the financial well being of your family.

Setting up the Family Trust...

Setting up the Family Trust was quite similar to setting up an SMSF, in the it consisted of:

The cost of setting up the Family Trust was about the same as the SMSF, ie, a few grand, but it is definitely worth it. I may be wrong, but I doubt it. :-)

At about the same time that I setup my SMSF, at the advice of my accountant, I also setup a Family Trust.

A Family Trust is similar in structure to the SMSF, in the sense that it a legal entity, essentially created by the existence of a deed document. It can own assets.

So, why setup a Family Trust?

A Family Trust allows me to distribute any income received by the Family Trust to the beneficiaries of the Trust in a discretionary manner. The beneficiaries of the Trust are the people (generally immediate family members) that can receive income generated by the Trust.

The real advantage of the Family Trust is the discretionary nature by which income can be allocated. Basically, income can be allocated as required (or, at the sole discretion of the Trustees) as to maximize the net benefit (ie, after tax) to the beneficiaries.

So, in my case, my partner and I will likely alternate being the primary income earner and the primary care giver across a number of years. Using the Family Trust structure, we simply put the name of the income earning assets into the name of the Trust, and can then (in any given tax year, and changing between tax years) allocate income to primary care giver first, ensure that we maximize our net earnings.

We can also allocate $3,000 per year to each child, without paying any tax on that income.

You should be able to see the effectiveness of the Family Trust structure, in building and maintaining the financial well being of your family.

Setting up the Family Trust...

Setting up the Family Trust was quite similar to setting up an SMSF, in the it consisted of:

- Creating the Trust Deed document, which, amongst other things, contained the list of Trustees (the people that control the Trust), the list of Beneficiaries (the people that benefit from the Trust).

- Getting ABNs and TFNs for the Trust

- Setting up bank accounts in the name of the Trust.

- Moving existing assets into the name of the Trust.

- Had over $100,000 in funds to manage.

- Had family members that were either temporarily or permanently in lower tax brackets.

- Had at least one child, although the more the better.

The cost of setting up the Family Trust was about the same as the SMSF, ie, a few grand, but it is definitely worth it. I may be wrong, but I doubt it. :-)

The tortoise and the hare

There are 2 types of investors - tortoises and hares. Nearly everything taught and written about investing these days is written for hares, by hares. After all, the hares wear the best suits, have the best jobs, drive the fastest cars, etc. The tortoises, however, have more wealth.

As the race starts, the hare bolts out of the blocks as fast as he can, and heads where all the other hares are going. The tortoise, on the other hand, heads for the wall that contains the train timetable, carefully studies it and plans out his route. He then heads for the station, and sits and waits at the platform. He realises that, although it doesn't look particularly exciting, waiting at the platform for the train will ultimately lead him to the finish line in the fastest possible time. There are lots of hares that run past this particular station, and they all laugh at the tortoise - just sitting there. The tortoise is actually reading while he waits. He is of course planning out what to do once he gets off the train.

Eventually, after what seems like an eternity, the train arrives, and the tortoise boards. Even then, however, the hares laugh at him. For the train takes off so slowly that the hares are still able to run straight passed. The tortoise doesn't notice though, as he has his head down and is reading some more.

The hares stop laughing as it starts to rain. The hares don't like the rain. They turn around and scamper to the last comfortable indoor place they passed to wait out the rain. If the hare hadn't have been on the train, the rain wouldn't have bothered him anyway. He always carries an umbrella - just in case. The hares laugh at him for this too.

Anway, the train that started slowly, has ever so surely been picking up speed as is now moving along very fast. The tortoise looks out the window and sees that the train is moving faster than any of the hares. He then looks around the inside of the train. He notices a few other tortoises on in carriage - some of which he recognises, and some of which he doesn't. Those that know each other, give their friends a wry smile, and then they all go back to their reading.

To be continued...

As the race starts, the hare bolts out of the blocks as fast as he can, and heads where all the other hares are going. The tortoise, on the other hand, heads for the wall that contains the train timetable, carefully studies it and plans out his route. He then heads for the station, and sits and waits at the platform. He realises that, although it doesn't look particularly exciting, waiting at the platform for the train will ultimately lead him to the finish line in the fastest possible time. There are lots of hares that run past this particular station, and they all laugh at the tortoise - just sitting there. The tortoise is actually reading while he waits. He is of course planning out what to do once he gets off the train.

Eventually, after what seems like an eternity, the train arrives, and the tortoise boards. Even then, however, the hares laugh at him. For the train takes off so slowly that the hares are still able to run straight passed. The tortoise doesn't notice though, as he has his head down and is reading some more.

The hares stop laughing as it starts to rain. The hares don't like the rain. They turn around and scamper to the last comfortable indoor place they passed to wait out the rain. If the hare hadn't have been on the train, the rain wouldn't have bothered him anyway. He always carries an umbrella - just in case. The hares laugh at him for this too.

Anway, the train that started slowly, has ever so surely been picking up speed as is now moving along very fast. The tortoise looks out the window and sees that the train is moving faster than any of the hares. He then looks around the inside of the train. He notices a few other tortoises on in carriage - some of which he recognises, and some of which he doesn't. Those that know each other, give their friends a wry smile, and then they all go back to their reading.

To be continued...

Definitions

A friend once told me that it was silly to argue over definitions. I understand his point. If someone starts a conversation with "Let X be blah..", there is no point arguing: "No it's not".

However, what you can argue about definitions is whether or not they are commonly accepted, or, more precisely, how commonly accepted they are.

The other thing you can argue is the usefulness of a particular definition. For example, defining "black" as "white" isn't particularly useful.

So, given various options for a particular definition I will favor usefulness over acceptance.

However, what you can argue about definitions is whether or not they are commonly accepted, or, more precisely, how commonly accepted they are.

The other thing you can argue is the usefulness of a particular definition. For example, defining "black" as "white" isn't particularly useful.

So, given various options for a particular definition I will favor usefulness over acceptance.

Is your family home an investment?

I lost this argument the other night, but I'm still sure that I'm right.

The question was whether or not you should consider your primary residence an investment. I think that you should, but I couldn't convince anyone else.

Say, for example, that you have $500,000 that you are currently managing through various investments. If you use this money to buy your family home, does it suddenly not become an investment? If not, where did that investment go? How do I report on that portfolio?

Of course, if I let someone else live in this home and pay me rent, then it's suddenly becomes an investment, obviously, and, even if I leave it vacant, it is still an investment. Yet, for some reason, the moment that I walk into it with a pillow, it is no longer an investment.

That is, of course, unless I happen to sell it some years later for a profit, at which point, people will say "You made a great investment there".

This argument actually came up during a conversation about current house prices in Australia, and whether or not now was a good time to buy a house. I think it was raised by the housing bull, as a last ditched effort to justify buying in the current climate - that is, at the peak of the housing bubble.

Having been pounded by arguments against the possibility of rising house prices in the coming years, he resorted to "but you shouldn't consider your primary residence as an investment".

Right, I get it now. So, because it isn't an investment, I can then justify the 30% capital loss. Pure genius - or slightly delusional.

The question was whether or not you should consider your primary residence an investment. I think that you should, but I couldn't convince anyone else.

Say, for example, that you have $500,000 that you are currently managing through various investments. If you use this money to buy your family home, does it suddenly not become an investment? If not, where did that investment go? How do I report on that portfolio?

Of course, if I let someone else live in this home and pay me rent, then it's suddenly becomes an investment, obviously, and, even if I leave it vacant, it is still an investment. Yet, for some reason, the moment that I walk into it with a pillow, it is no longer an investment.

That is, of course, unless I happen to sell it some years later for a profit, at which point, people will say "You made a great investment there".

This argument actually came up during a conversation about current house prices in Australia, and whether or not now was a good time to buy a house. I think it was raised by the housing bull, as a last ditched effort to justify buying in the current climate - that is, at the peak of the housing bubble.

Having been pounded by arguments against the possibility of rising house prices in the coming years, he resorted to "but you shouldn't consider your primary residence as an investment".

Right, I get it now. So, because it isn't an investment, I can then justify the 30% capital loss. Pure genius - or slightly delusional.

Predictions for the Australian Housing Market Bubble

Wow - an Australian first. A dinner party discussion about the Australian housing market where the bears outnumbered the bulls. It was incredible. One only needs to go back a couple of years and it would have been the unanimous position that house prices in Australian could not go down, let alone that Australian house prices would go down.

The arguments given by the lone bull were the pretty typical, but we weren't convinced. We knew all about the Australian Housing Market Myths.

Anyway, for posterity, I thought I'd put the survey results here. The question was on the change in the median Melbourne house price over the coming years.

Now, I would never use a voting system to determine correctness on a given issue, as usually I'm the delusional one getting out-voted. However, from the survey results above we can conclude one thing for sure - at least 1 person at the table was delusional.

The arguments given by the lone bull were the pretty typical, but we weren't convinced. We knew all about the Australian Housing Market Myths.

Anyway, for posterity, I thought I'd put the survey results here. The question was on the change in the median Melbourne house price over the coming years.

| Person A | Person B | Person C | Person D | Person E | |

|---|---|---|---|---|---|

| 1 year | 0 | -10% | 0 | -5% | 0 |

| 2 year | +10% to +15% | -15% | -15% | -10% | -10% |

| 3 year | +17% to +35% | -25% to -30% | -30% | -15% | -15% |

Now, I would never use a voting system to determine correctness on a given issue, as usually I'm the delusional one getting out-voted. However, from the survey results above we can conclude one thing for sure - at least 1 person at the table was delusional.

Self Managed Superannuation

Having cunningly devised what I believed to be a great investment strategy, I needed some capital to put it to the test. Fortunately, in Australia, there is this thing called superannuation, which is basically legally enforced retirement savings.

Like most youngish people, I had paid little to no attention to super, despite the fact that it is my money. The commercial super companies love people like me. I had changed jobs several times, had multiple super funds with multiple fund managers, and they creamed all the fees they could.

I was also quite bearish about 2010, and so was uncomfortable letting someone else manage my money.

So, I started looking into setting up my own self managed super fund (SMSF), which turned out relatively straight forward.

The first step was consolidating all my super funds with a single fund manager, and changing the fund profile to "Cash". Hopefully, this would protect me in the event of another stock market crash whilst I was setting up the SMSF.