One of the things that makes it difficult is that it's a different answer depending on whether we are talking about an individual company verses an equity index (eg. ASX All Ords).

Let's start with what appears to be the most obvious answer - profitability. The most significant factor affecting the share price of an individual company, and perhaps even the indexes, are their profitability. In general, the more profitable companies are, the higher price they can command.

And what is the most significant factor affecting companies profitability? Over the long term, as Buffett discovered, the answer to this is degree to which to the company has a durable competitive advantage. One of the best examples of a company with a durable competitive advantage is Coca Cola. Buffett has said that even if he had a billion dollars dedicated to sinking Coca Cola, he couldn't do it. This durable competitive advantage enables the company to raise its prices at a rate faster than inflation, maintain higher profit margins than it's competitors, and therefore create more earnings for it's shareholders. In Buffett's own words:

The single most important decision in evaluating a business is pricing power. If you’ve got the power to raise prices without losing business to a competitor, you’ve got a very good business. And if you have to have a prayer session before raising the price by 10 percent, then you’ve got a terrible business

So that's the answer for individual companies, but what about the markets as a whole? What are the most significant factors that affect the market indices. There are many candidates, including news announcements, reserve bank rate changes, political events, etc. For example, take a look at the following graph, created by Avid Chartist, that shows the relationship between the US stock market and the AU stock market.

Over longer time frames, however, it is the comparable rate of returns of other asset classes that determine the price investors are willing to pay for a given set of earnings. If, *cough*, safe haven investments such as government bonds have higher rates of return, then capital will flow into these bonds, lower the prices of the equity markets, and hence, eventually, equalizing the return disparity.

The real problem that exists today, is that it is not free markets that determine rates of return on government bonds. Instead, it is central bank policy that determines the government bond interest rates, which naturally determines the bond market prices. Thus the comparable rates of returns for equities are artificially low, and the price is artificially high.

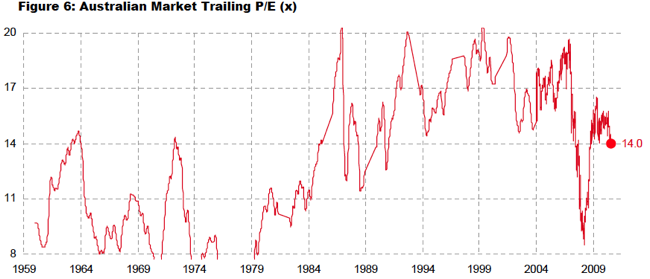

Consider the following:

Should the central banks ever lose control of these interest rates (a topic with enough meat for another post), one could reasonably expect that rates of return would return to their historical levels (10%), if not overshoot somewhat in the short term (16%).

Assuming that earnings remained stable, this would require equity price drops of 40% to 80%. Perhaps the sniper should be more patient.

No comments:

Post a Comment