A friend and colleague recently described my investing strategy back to me as sniping. I had chosen my target companies, and for each one of them I had identified a target price. The cross-hairs were set and I was ready. The trigger finger was not particularly twitchy, but it was ready to fire the moment that something appeared in the sights.

Anyway, I recently went traveling, and so was pretty much off line for about a month. Knowing that this was going to be the case, I decided that I'd put in some low-ball buy orders on the market before I went, just in case a stock market crash occurred while I was away. I won't be so bold as to say that that was a prediction - well - the crash was, but not the timing.

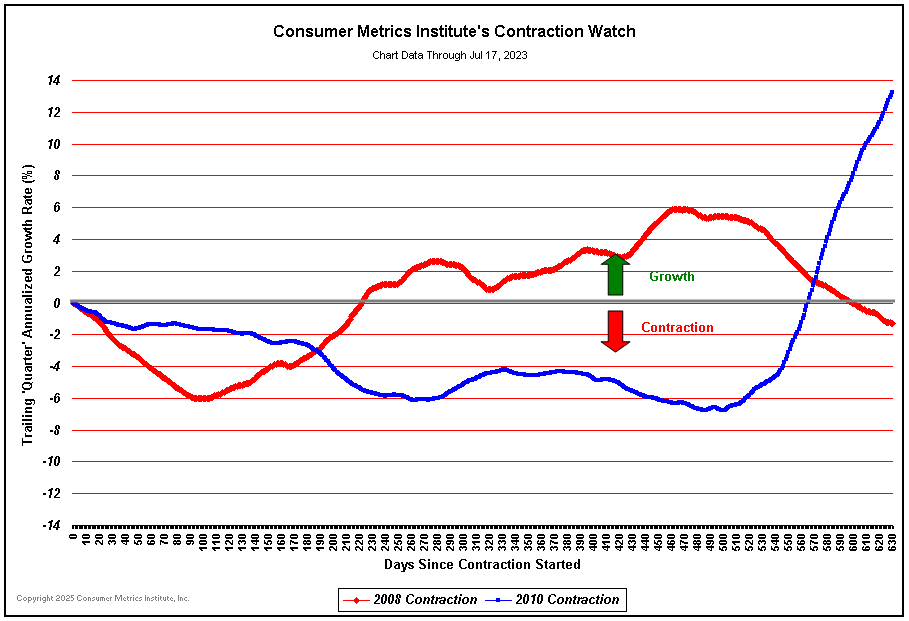

July Consumer Metrics data

I've long been a fan of the Comsumer Metrics Institute. They've been showing the US consumer "double dip" recession for well over a year now - yet the official numbers have only just been "adjusted" to reflect this.

Looking at the latest data, it is surprising to see an uptick that may indicate the end of the contraction.

Perhaps there is light at the end of the tunnel. Time will tell. The Consumer Metrics Institute will probably give a leading indicator either way..

Looking at the latest data, it is surprising to see an uptick that may indicate the end of the contraction.

Perhaps there is light at the end of the tunnel. Time will tell. The Consumer Metrics Institute will probably give a leading indicator either way..

Antal Fekete

Fekete's articles - an interesting read on gold, futures, and what the USD end game might look like.

Gold and Silver prices - Significant factors affecting

Following on from my look at the most significant factors affecting house prices, I would now like to take a look at the gold and silver, and the factors that most affect their prices. (Update: See also: significant factors affecting share prices).

Like with house prices, I'm trying to determine what has the largest impact on their price over the long term, rather than the factors that cause their volatility, as I'm long term investor.

I don't claim to be an expert on the precious metals, but that's never stopped me from having an investment opinion before, so here goes.

Like with house prices, I'm trying to determine what has the largest impact on their price over the long term, rather than the factors that cause their volatility, as I'm long term investor.

I don't claim to be an expert on the precious metals, but that's never stopped me from having an investment opinion before, so here goes.

House Prices - Significant Factors

My plan is to make this a multi-part series, where I take a look at various classes of assets, and the most significant factors that determine or influence their prices. Today I'll look at house prices. Later, I'll take a look at stock market share prices (Update: See here), and I also hope to take a look at gold and silver prices at some stage as well (Update: See here).

So, what are the factors that affect house prices, in order of significance? As an investor, and as a potential home owner, understanding these factors are crucial to making a sensible and profitable investment decision, yet the answers far from clear, and rarely understood. Here's my take on it.

So, what are the factors that affect house prices, in order of significance? As an investor, and as a potential home owner, understanding these factors are crucial to making a sensible and profitable investment decision, yet the answers far from clear, and rarely understood. Here's my take on it.

The problem with "averaging in"

A popular approach to buying shares is set "buy" thresholds. It's a fairly simple approach - when the share prices falls to reach the threshold price, you buy some shares. Often, there are multiple buy point thresholds, such that as the share price falls through each of the threshold, you buy more shares. The theory is that if you thought that the share price was cheap at say $5, then when it hits $4.50, it must be even better value, and so a better buying opportunity.

The theory is not wrong, it is just not optimal.

The theory is not wrong, it is just not optimal.

The Term Deposit Investing Model

It's been a while, so here's another thought experiment.

Suppose that a bank occasionally offered term deposit accounts at extraordinarily good interest rates - say 20% (for ever). Suppose also, that they only did so very rarely - once every 5-10 years. The catch is of course that it's very difficult to get money into this term deposit, as they only accept small denominations, so you have to manually keep filling out application forms so that you can get as much money in as possible, and you have to do so for the limited time that the bank will accept the applications.

Suppose that a bank occasionally offered term deposit accounts at extraordinarily good interest rates - say 20% (for ever). Suppose also, that they only did so very rarely - once every 5-10 years. The catch is of course that it's very difficult to get money into this term deposit, as they only accept small denominations, so you have to manually keep filling out application forms so that you can get as much money in as possible, and you have to do so for the limited time that the bank will accept the applications.

Getting left behind

Another dinner party on the weekend, and so another chance to make some observations about people's beliefs about the Australian property market.

One guy made the (somewhat typical) following comments:

One guy made the (somewhat typical) following comments:

- If you don't buy now, you're going to get left behind.

- If not now, then when? Prices are only going to go up.

Price to Book ratio and Return on Equity

Following on from my look at the Price to Earnings ratio, and in a similar vein to my post on subsequent rates of return, I'd now like to take a look at P/B ratios and ROE. The mechanics of the numbers are fairly straight forward.

The Price to Book ratio is the price that you pay for the book value of the company - the book value being the net (booked) value of their assets - or in really simplistic terms - how much money they have in the bank, assuming no liabilities. So, if they have $100,000 in assets and you pay $200,000 for the company, you are paying a price to book value of 2:1.

The Return on Equity is simply how efficient the company is at making a profit. If they use the $100,000 to generate $15,000 profit, they have an ROE of 15%. Not bad.

These two metrics are linked though the P/E ratio.

The Price to Book ratio is the price that you pay for the book value of the company - the book value being the net (booked) value of their assets - or in really simplistic terms - how much money they have in the bank, assuming no liabilities. So, if they have $100,000 in assets and you pay $200,000 for the company, you are paying a price to book value of 2:1.

The Return on Equity is simply how efficient the company is at making a profit. If they use the $100,000 to generate $15,000 profit, they have an ROE of 15%. Not bad.

These two metrics are linked though the P/E ratio.

Subscribe to:

Posts (Atom)

{kind=link}